As I reveal my ignorance about TikTok trends, social media celebrities and Gen Z slang, my children are quick to point out my age, and I accept that reality, for the most part. I understand that I am too old to exercise without stretching first or eat a heaping plate of cheese fries and not suffer heartburn, but that does not stop me from trying occasionally. For the last decade or so, I have argued that businesses, like human beings, age, and struggle with aging, and that much of the dysfunction we observe in their decision making stems from refusing to act their age. In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book. While the writing for the book was largely done by November 2022, publishing does have a long lead time, and the book, published by Penguin Random House, will be available on August 20, 2024, at a book shop near you. If you are concerned that you are going to be hit with a sales pitch for that book, far from it! Rather than try to part you from your money, I thought I would give a compressed version of the book in this post, and for most of you, that will suffice.

Setting the Stage

{kind=link}

Measures and Determinants

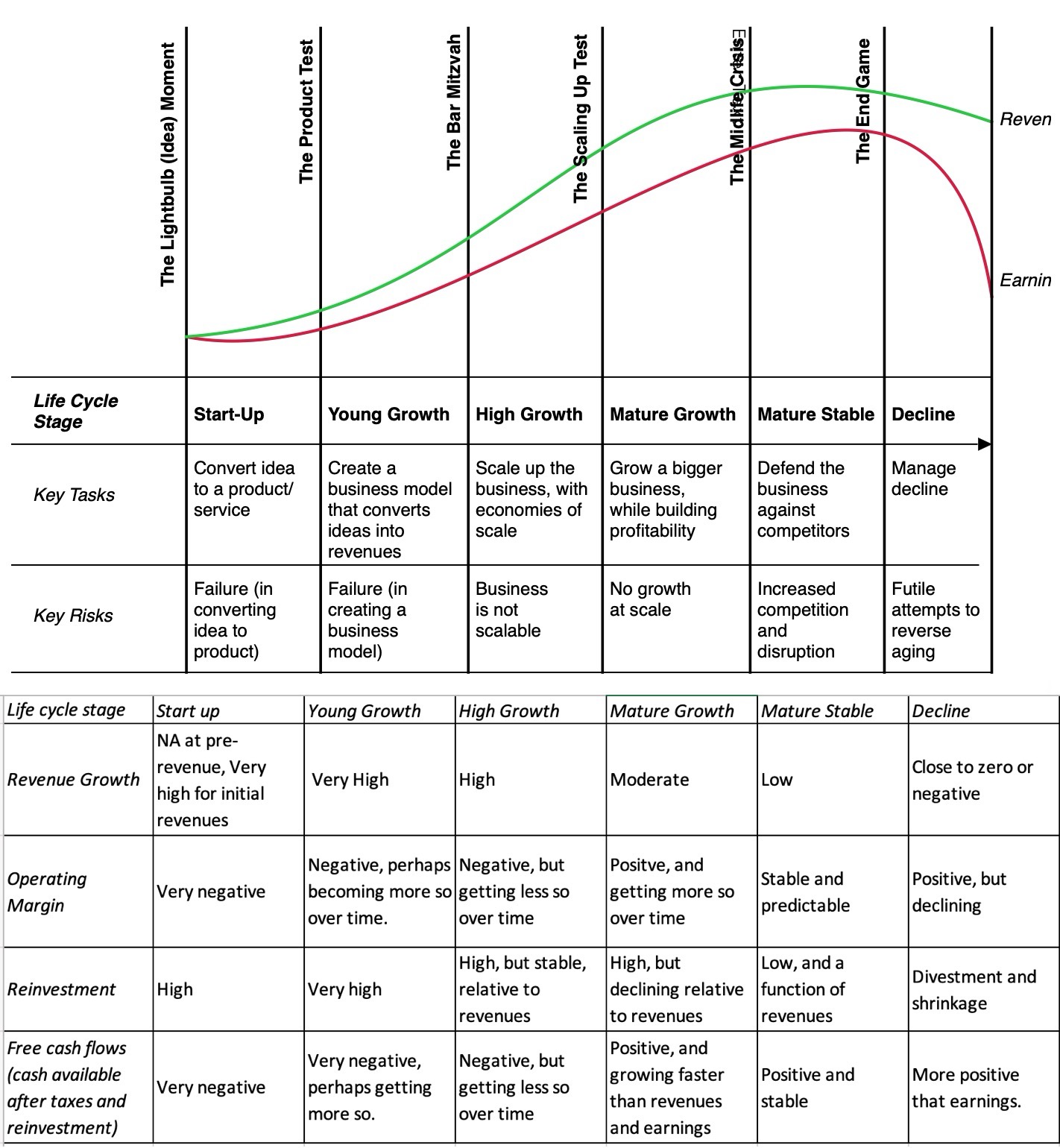

If you buy into the notion of a corporate life cycle, it stands to reason that you would like a way to determine where a company stands in the life cycle. There are three choices, each with pluses and minuses.

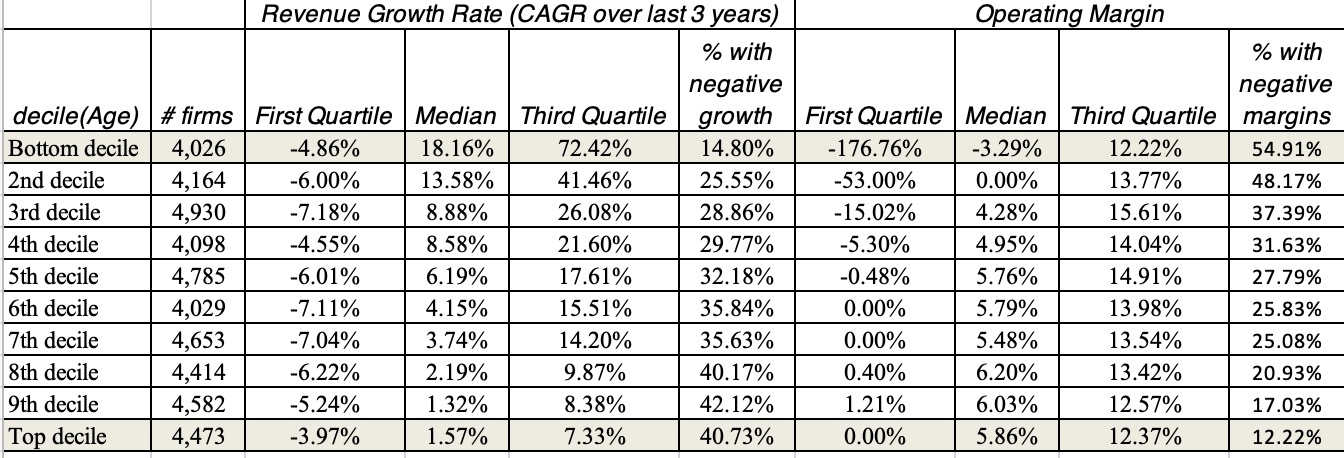

The first is to focus on corporate age, where you estimate how old a company is, relative its founding date; it is easy to obtain, but companies age at different rates (as well will argue in the following section), making it a blunt weapon.The second is to look at the industry group or sector that a company is in, and then follow up by classifying that industry group or sector into high or low growth; for the last four decades, in US equity markets, tech has been viewed as growth and utilities as mature. Here again, the problem is that high growth industry groups begin to mature, just as companies do, and this has been true for some segments of the tech sector.The third is to focus on the operating metrics of the firm, with firms that deliver high revenue growth, with low/negative profits and negative free cash flows being treated as young firms. It is more data-intensive, since making a judgment on what comprises high (revenue growth or margins) requires estimating these metrics across all firms.While I delve into the details of all three measures, corporate age works surprisingly well as a proxy for where a company falls in the life cycle, as can be seen in this table of all publicly traded companies listed globally, broken down by corporate age into ten deciles:

{kind=link}

As you can see, the youngest companies have much higher revenue growth and more negative operating margins than older companies.

Ultimately, the life cycles for companies can vary on three dimensions – length (how long a business lasts), height (how much it can scale up before it plateaus) and slope (how quickly it can scale up). Even a cursory glance at the companies that surround you should tell you that there are wide variations across companies, on these dimensions. To see why, consider the factors that determine these life cycle dimensions:

{kind=link}

The drivers of the corporate life cycle can also explain why the typical twenty-first century company faces a compressed life cycle, relative to its twentieth century counterpart. In the manufacturing-centered twentieth century, it took decades for companies like GE and Ford to scale up, but they also stayed at the top for long periods, before declining over decades. The tech-centered economy that we live in is dominated by companies that can scale up quickly, but they have brief periods at the top and scale down just as fast. Yahoo! and BlackBerry soared from start ups to being worth tens of billions of dollars in a blink of an eye, had brief reigns at the top and melted down to nothing almost as quickly.

{kind=link}

Corporate Finance across the Life Cycle

Corporate finance, as a discipline, lays out the first principles that govern how to run a business, and with a focus on maximizing value, all decisions that a business makes can be categorized into investing (deciding what assets/projects to invest in), financing (choosing a mix of debt and equity, as well as debt type) and dividend decisions (determining how much, if any, cash to return to owners, and in what form).

{kind=link}

{kind=link}

Valuation across the Life Cycle

I am fascinated by valuation, and the link between the value of a business and its fundamentals – cash flows, growth and risk. I am also a realist and recognize that I live in a world, where pricing dominates, with what you pay for a company or asset being determined by what others are paying for similar companies and assets:

{kind=link}

{kind=link}

{kind=link}

Investing across the Life Cycle

In my class (and book) on investment philosophies, I start by noting that every investment philosophy is rooted in a belief about markets making (and correcting) mistakes, and that there is no one best philosophy for all investors. I use the investment process, starting with asset allocation, moving to stock/asset selection and ending with execution to show the range of views that investors bring to the game:

{kind=link}

{kind=link}

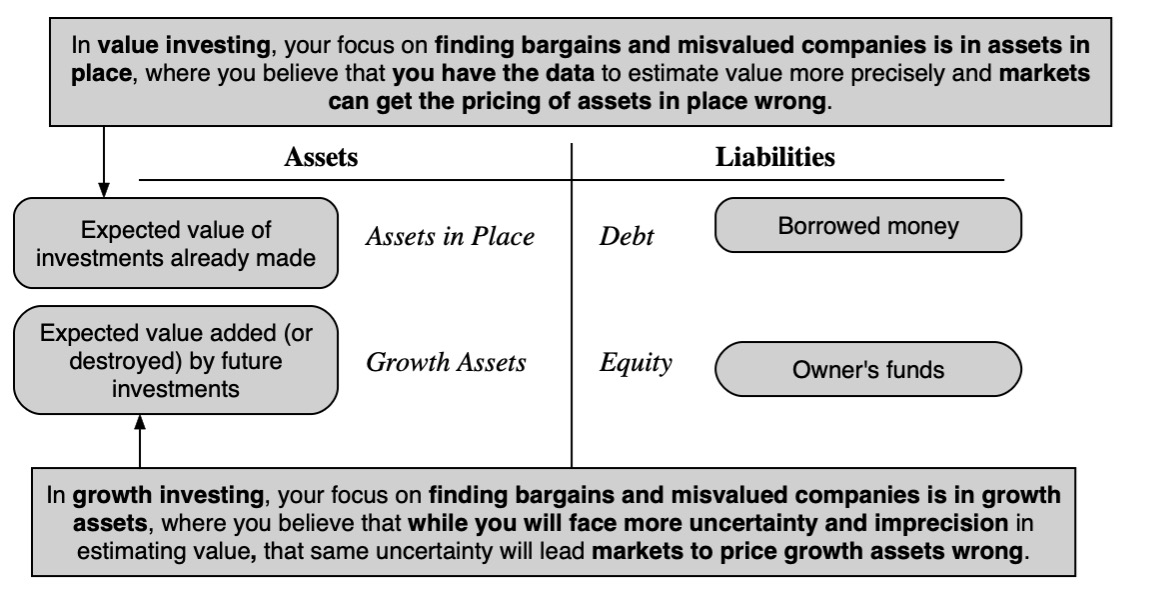

Value investors believe that the best investment bargains are in mature companies, where assets in place (investments already made) are being underpriced by the market, whereas growth investors build their investment theses around the idea that it is growth assets where markets make mistakes. Finally, there are market players who try to make money from market frictions, by locking in market mispricing (with pure or near arbitrage).

Drawing on the earlier discussion of value versus price, you can classify market players into investors (who value companies, and try to buy them at a lower price, while hoping that the gap closes) and traders (who make them money on the pricing game, buying at a low price and selling at a higher one). While investors and traders are part of the market in every company, you are likely to see the balance between the two groups shift as companies move through the life cycle:

{kind=link}

In sum, the investment philosophy you choose can lead you to over invest in companies in some phases of the life cycle, and while that by itself is not a problem, denying that this skew exists can become one. Thus, deep value investing, where you buy stocks that trade at low multiples of earnings and book value, will result in larger portions of the portfolio being invested in mature and declining companies. That portfolio will have the benefit of stability, but expecting it to contain ten-baggers and hundred-baggers is a reach. In contrast, a venture capital portfolio, invested almost entirely in very young companies, will have a large number of wipeouts, but it can still outperform, if it has a few large winners. Advice on concentrating your portfolio and having a margin of safety, both value investing nostrums, may work with the former but not with the latter.

Managing across the Life Cycle

Management experts who teach at business schools and populate the premier consulting firms have much to gain by propagating the myth that there is a prototype for a great CEO. After all, it gives them a reason to charge nose-bleed prices for an MBA (to be imbued with these qualities) or for consulting advice, with the same end game. The truth is that there is no one-size-fits-all for a great CEO, since the qualities that you are looking for in top management will shift as companies age:

{kind=link}

{kind=link}

Aging gracefully?

The healthiest response to aging is acceptance, where a business accepts where it is in the life cycle, and behaves accordingly. Thus, a young firm that derives much of its value from future growth should not put that at risk by borrowing money or by buying back stock, just as a mature firm, where value comes from its existing assets and competitive advantages, should not risk that value by acquiring companies in new and unfamiliar businesses, in an attempt to return to its growth days. Acceptance is most difficult for declining firms, since the management and investors have to make peace with downsizing the firm. For these firms, it is worth emphasizing that acceptance does not imply passivity, a distorted and defeatist view of karma, where you do nothing in the face of decline, but requires actions that allow the firm to navigate the process with the least pain and most value to its stakeholders.

It should come as no surprise that many firms, especially in decline, choose denial, where managers and investors come up with excuses for poor performance and lay blame on outside factors. On this path, declining firms will continue to act the way they did when they were mature or even growth companies, with large costs to everyone involved. When the promised turnaround does not ensue, desperation becomes the alternative path, with managers gambling large sums of other people’s money on long shots, with predictable results.

The siren song that draws declining firms to make these attempts to recreate themselves, is the hope of a rebirth, and an ecosystem of bankers and consultants offers them magic potions (taking the form of proprietary acronyms that either restate the obvious or are built on foundations of made-up data) that will make them young again. They are aided and abetted by case studies of companies that found pathways to reincarnation (IBM in 1992, Apple in 2000 and Microsoft in 2013), with the added bonus that their CEOs were elevated to legendary status. While it is undeniable that companies do sometimes reincarnate, it is worth recognizing that they remain the exception rather than the rule, and while their top management deserves plaudits, luck played a key role as well.

I am a skeptic on sustainability, at least as applied to companies, since its makes corporate survival the end game, sometimes with substantial costs for many stakeholders, as well as for society. Like the Egyptian Pharaohs who sought immortality by wrapping their bodies in bandages and being buried with their favorite possessions, companies that seek to live forever will become mummies (and sometimes zombies), sucking up resources that could be better used elsewhere.

In conclusion

It is the dream, in every discipline, to come up with a theory or construct that explains everything in that disciple. Unlike the physical sciences, where that search is constrained by the laws of nature, the social sciences reflect more trial and error, with the unpredictability of human nature being the wild card. In finance, a discipline that started as an offshoot of economics in the 1950s, that search began with theory-based models, with portfolio theory and the CAPM, veered into data-based constructs (proxy models, factor analysis), and behavioral finance, with its marriage of finance and psychology. I am grateful for those contributions, but the corporate life cycle has offered me a low-tech, but surprisingly wide reaching, construct to explain much of what I see in business and investment behavior.

If you find yourself interested in the topic, you can try the book, and in the interests of making it accessible to a diverse reader base, I have tried to make it both modular and self-standing. Thus, if you are interested in how running a business changes, as it ages, you can focus on the four chapters that look at corporate finance implications, with the lead-in chapter providing you enough of a corporate finance foundation (even if you have never taken a corporate finance class) to be able to understand the investing, financing and dividend effects. If you are an appraiser or analyst, interested in valuing companies across the life cycle, it is the five chapters on valuation that may draw your interest, again with a lead-in chapter containing an introduction to valuation and pricing. As an investor, no matter what your investment philosophy, it is the four chapters on investing across the life cycle that may appeal to you the most. While I am sure that you will have no trouble finding the book, I have a list of book retailers listed below that you can use, if you choose, and the webpage supporting the book can be found here.

If you are budget-constrained or just don’t like reading (and there is no shame in that), I have also created an online class, with twenty sessions of 25-35 minutes apiece, that delivers the material from the book. It includes exercises that you can use to check your understanding, and the link to the class is here.

YouTube Video

Book and Class Webpages

Book webpage: https://pages.stern.nyu.edu/~adamodar//New_Home_Page/CLC.htmClass webpage: https://pages.stern.nyu.edu/~adamodar//New_Home_Page/webcastCLC.htmYouTube Playlist for class: https://www.youtube.com/playlist?list=PLUkh9m2BorqlpbJBd26UEawPHk0k9y04_

Links to booksellers

Amazon: https://www.amazon.com/Corporate-Lifecycle-Investment-Management-Implications/dp/0593545060Barnes & Noble: https://www.barnesandnoble.com/w/the-corporate-life-cycle-aswath-damodaran/1143170651?ean=9780593545065Bookshop.org: https://bookshop.org/p/books/the-corporate-lifecycle-business-investment-and-management-implications-aswath-damodaran/19850366?ean=9780593545065Apple: https://books.apple.com/us/audiobook/the-corporate-life-cycle-business-investment/id1680865376(There is an Indian edition that will be released in September, which should be available in bookstores there.)